Tax Changes 2025-2026

The 2025 One, Big, Beautiful Bill Act (OBBBA) will decrease the amount of a charitable gift, including those to church, that can be used as an itemized deduction in 2026.

The full amount of a gift made in 2025 is eligible as an itemized deduction for most taxpayers. Beginning in 2026, the gift amount that is eligible as an itemized deduction will be reduced based on the adjusted gross income of the donor(s).

The Christian Church Foundation does not provide tax or legal advice and the information offered here is solely informational. Many factors affect each taxpayers’ options and eligibility for income tax deductions. The Gift Deductions Comparison chart and examples are provided as information only.

You may also share this page directly to your members or donors https://christianchurchfoundation.org/tax-changes/

Below are two articles that may be used in your ministry to help others understand these tax changes

Maximize Tax Deductions 2025 – New Tax Code 2026

Tax code changes from the 2025 One, Big, Beautiful Bill Act (OBBBA) will affect the income tax deductible amount that may be available from charitable giving, including gifts to the church.

Beginning in 2026, itemizing taxpayers can only deduct charitable contributions that exceed 0.5 percent of their adjusted gross income (AGI).

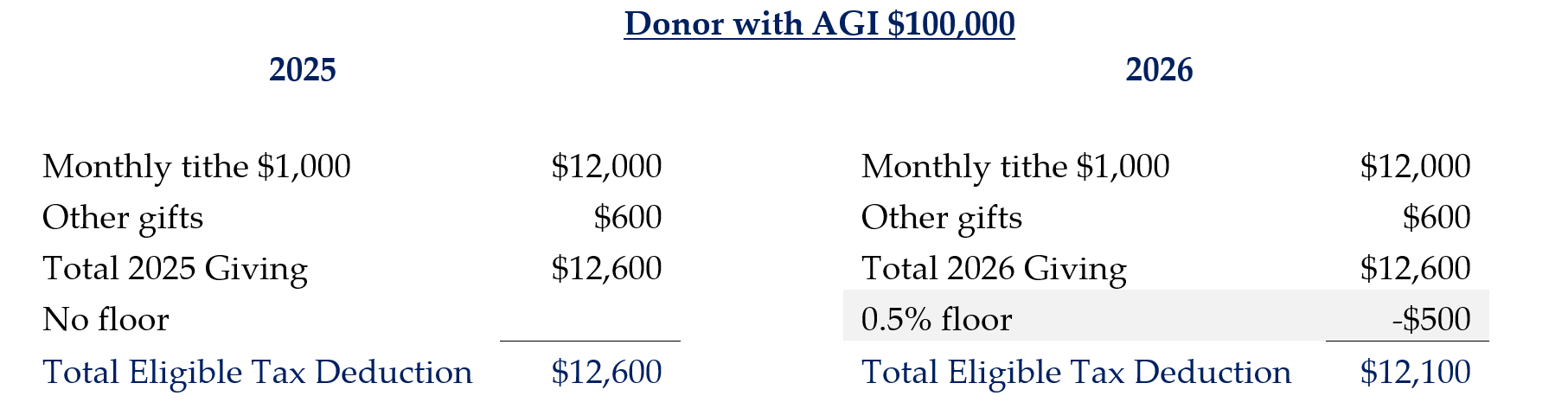

To illustrate this, here is a very simple example of how the new ‘giving floor’ will work in 2026. A donor with an AGI of $100,000 will have a ‘giving floor’ of $500. (100,000 x .005 = 500). The first $500 of the donors’ combined annual gifts will not be eligible as a deduction; any amount above $500 is eligible.

Due to this change, donors may want to maximize their eligible tax deductions in 2025 by “bunching” their gifts in 2025 (for example, making a larger gift in 2025 that may represent two years of giving). For those taxpayers who itemize, the full amount of a gift made in 2025 will be an eligible income tax deduction for the 2025 tax year.

2025 Giving for 2026 Benefit

The Christian Church Foundation offers a Steward’s Donor Advised Fund, where contributions can be made in one year and distributed to the ministry/ministries of the donor’s choice in the year given or later years. Gifts to a Steward’s Donor Advised Fund in 2025 would be eligible for the full tax deduction with the opportunity to support ministry in 2025, 2026, or later. A minimum gift of $10,000 is needed to create a new Steward’s Donor Advised Fund.

Talk with a Foundation Zone representative to learn more about this or other changes to the tax code that may impact your stewardship, and consult your tax advisor for options tailored to your specific goals.

Remember, many factors affect each taxpayer’s options and eligibility for income tax deductions. The Christian Church Foundation does not provide tax or legal advice, and the information offered here is solely informational.

![]()

Tax Code changes will continue to affect charitable contributions

The 2017 Tax Cuts and Jobs Act lowered individual income tax rates, increased the standard deduction, capped the deduction for state and local taxes, and eliminated other itemized deductions. These changes significantly reduced the number of taxpayers itemizing their returns; and thereby, the number of taxpayers taking a deduction for their gifts to the church and other charitable contributions. The law also significantly raised the estate tax exemption removing tax incentives for estate gifts from some potential donors with larger estates.

A July 2024 report by researchers at Indiana University and the University of Notre Dame, looking specifically at the affect of higher standard deductions on giving, found that approximately 23 million households did not itemize their charitable deductions in 2017, instead taking the standard deduction in 2018. The research indicates that each of these non-itemizing households decreased their giving from 2017 by an average of $880, resulting in a cumulative decrease in charitable giving by approximately $20 billion in 2018. https://www.nber.org/papers/w32737

The One, Big, Beautiful Bill Act of 2025 will also affect charitable giving.

Standard Deductions

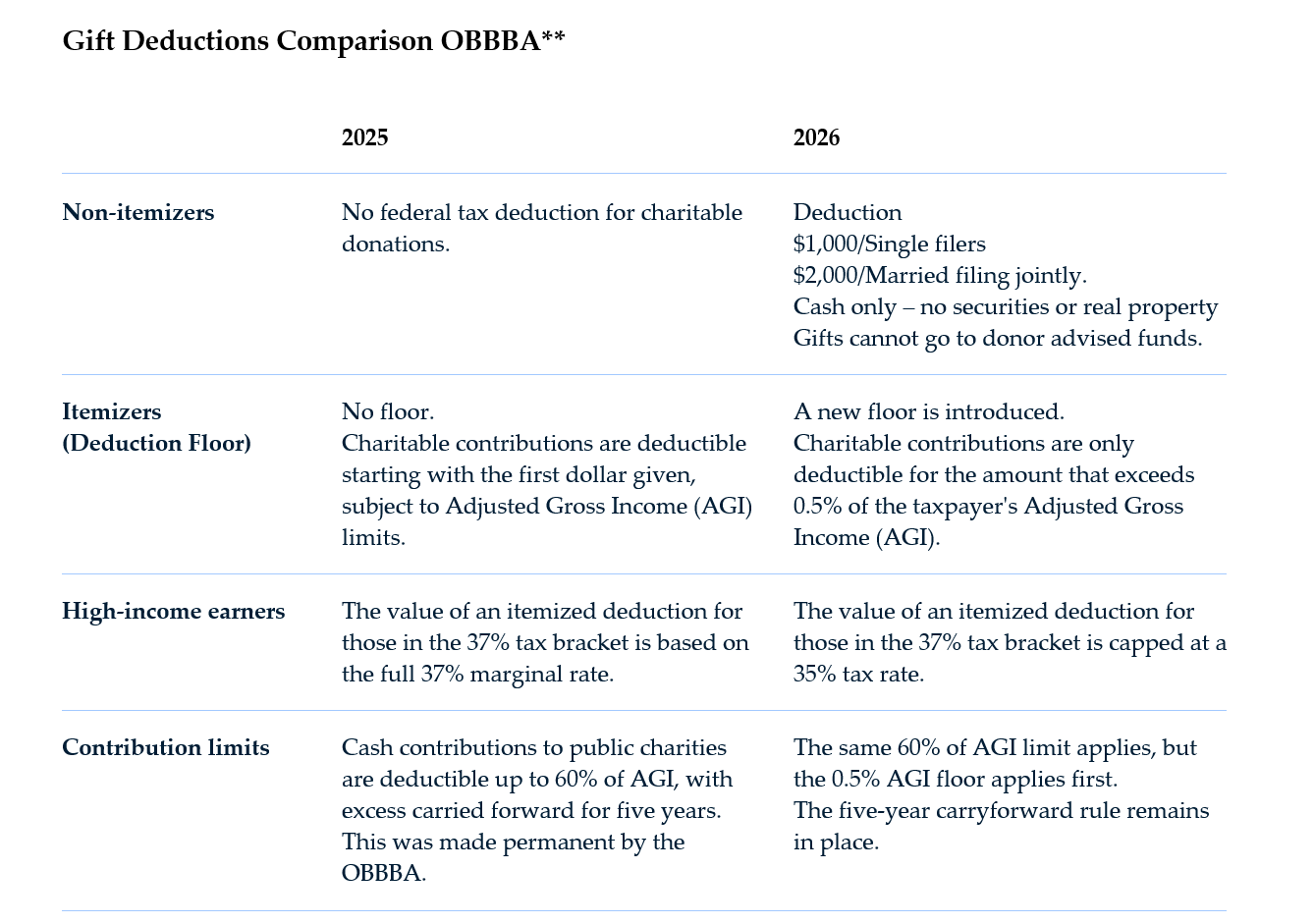

The One, Big, Beautiful Bill Act (OBBBA) further increased the standard deductions for 2025 with future standard deductions to be increased annually based on inflation.

Beginning in 2026, donors who utilize the standard deduction and do not itemize will be able to receive an additional deduction of $1,000 (single filers) or $2,000 (married filing jointly) for charitable gifts. This deduction is only applicable to cash gifts, not stocks, securities, or real property, and the gift cannot be contributed to a donor advised fund.

Itemized Deductions

Also beginning in 2026, the income tax deduction for itemized charitable gifts will be reduced by 0.5% of the taxpayers adjusted gross income. Additionally, donors in the highest tax brackets will only be allowed to claim 35% of their charitable gifts as deductions. While these changes may continue to discourage itemizing, which would include charitable giving, the Act increased the cap on the amount of state and local taxes that can be itemized (from $10,000 to $40,000). For some donors, itemizing their tax deductions, which could include medical expenses, state and local taxes, home mortgage interest, and charitable contributions, may provide a better tax option.

Achieving a tax benefit from giving is not restricted to itemizing or deductions; gifts from IRAs may help lower a donor’s overall adjusted gross income and, therefore, their overall tax burden.

The Zone representatives from the Christian Church Foundation are available to provide information to help donors consider how the changes to the tax code may affect their plans for giving in 2025 and 2026.

Every donor and every gift is unique. Please consult your tax advisor for options tailored to your specific goals.

The Christian Church Foundation does not provide tax or legal advice and the information offered here is solely informational.

Download PDF of tax change articles

![]()

** One, Big Beautiful Bill Act (OBBBA) became effective July 4, 2025, with some immediate changes and others changes that will occur in 2026 and later. Many factors affect each taxpayers’ options and eligibility for income tax deductions. The Christian Church Foundation does not provide tax or legal advice and the information offered here is solely informational.

Download Gift Deductions Comparison OBBBA Chart